LONDON (Reuters) - Financial markets rebounded on Tuesday, with stocks and oil jumping about 4% in Europe, while the safe-haven dollar recoiled as unprecedented global stimulus efforts gained traction.

Although the U.S. Federal Reserve’s offer of unlimited bond-buying was not expected to mitigate the devastating impact of the coronavirus alone, investors hoped it would help avert a global depression with the help of other state rescue packages.

The Fed’s action had not cheered Wall Street for long on Monday, with losses of 2%-3% on major indexes, but the mood improved on Tuesday, as other governments and central banks stepped in.

Wall Street S&P 500, Dow Jones and Nasdaq indexes were expected to bounce 4%, the main European bourses were up similar amounts and oil, gold and copper had all swung 3%-5% higher.

“Today there is a strong recovery connected to the move that the Fed has introduced this massive weapon,” said Francois Savary, CIO of wealth manager Prime Partners, adding the Fed needed to prioritize fixing the seize-ups in funding markets.

“The key issue at the end of the day is that we need to deal with a credit markets that is completely closed. First they needed to stop this increase in bond yields... second, they needed to make sure that there is a return of liquidity in the credit then it will be equities - in that sequence.”

Alongside buying unlimited amounts of assets, the Fed will also expand its mandate to corporate and municipal bonds and backstop a series of other measures that analysts estimate will deliver $4 trillion-plus in loans to non-financial firms.

There were also signs of progress in Congress on a $2 trillion U.S. stimulus deal, which Treasury Secretary Steven Mnuchin hoped was “very close”.

Other countries are unveiling their own measures. South Korea’s ravaged market climbed 8.6% after the government doubled a planned economic rescue package to 100 trillion won ($80 billion).

In China, mainland stocks posted their biggest gain in three weeks with a rise of almost 3%, while Japan’s Nikkei soared 7%, its biggest daily rise since February 2016.

But investors were still wary, as global coronavirus infections have topped 350,000 and China posted a rise in new infections brought in from abroad.

Japan said it was postponing the Olympics, General Motors became the latest to abandon its outlook for the year, while Ford had been the latest corporate giant to have its credit rating cut to the brink of ‘junk’ on Monday.

“Markets are continuing to bounce up on the latest policy announcements and then sliding back down as the economic reality of the situation re-emerges,” Deutsche Bank strategist Jim Reid said.

Euro zone business activity data collapsed to a record low on Tuesday and suffered by far its biggest one-month fall since the survey began in 1998.

But government and central bank financial support helped calm nerves in bond markets, where yields on two-year U.S. Treasuries hit their lowest since 2013. Ten-year yields were at 0.8339%, from last week’s peak of 1.28%.

Germany’s 10-year yield was up 2 basis points on the day at -0.36%, compared with a 4 bps rise before the purchasing managers index (PMI) releases, all small moves when compared to record lows hit at -0.90% earlier in March.

“I think we have reached some kind of equilibrium trading range in safe havens,” said DZ Bank strategist Rene Albrecht.

“Given the prospect for the economic downturn and much more (debt) issuance going forward, I think the level where yields are settling down is the place for them to be.”

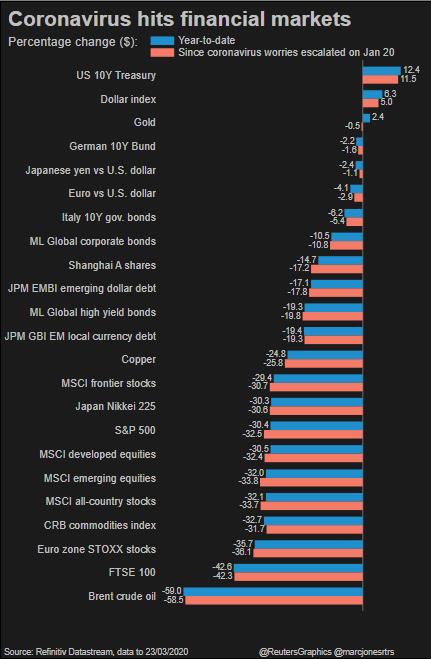

(Graphic: Global financial markets since coronavirus escalated, here)

{kind=link}

ALL ABOUT THE ECONOMY

The impact of the virus on the global economy is evident in a series of growth forecast downgrades and advance readings of PMIs across the world’s biggest economies.

German activity plunged to the lowest since the 2009 crisis, driven by a record services contraction, while French activity hit all-time lows. Japan posted its biggest-ever services fall.

“Economies around the world are going offline and that is devastating for economic activity, it’s creating the most robust dislocation in financial markets in living memory,” said George Boubouras, head of research at K2 Asset Management in Melbourne.

However, the prospect of massive Fed funding pushed the greenback 0.8% lower against rivals, off three-year peaks, falling against the yen and sliding 1% versus the euro.

Commodity and emerging market currencies benefited, with the Australian dollar up as much 2% to $0.59315 and well off 17-year lows.

There was less market volatility too. A gauge of expected euro-dollar swings eased below 12%, from above 14% on Monday, and a measure of U.S. equity volatility slipped to one-week lows around 55 points.

(Graphic: Volatility is back on Wall Street png, here)

{kind=link}

(Graphic: China's coronavirus cases JPG, here)

{kind=link}

Reporting by Sujata Rao; Additional reporting by Karin Strohecker and Yoruk Bahceli in London, Wayne Cole in Syndey and Scott Murdoch in Hong Kong; Editing by Alex Richardson and Edmund Blaair

https://news.google.com/__i/rss/rd/articles/CBMifWh0dHBzOi8vd3d3LnJldXRlcnMuY29tL2FydGljbGUvdXMtZ2xvYmFsLW1hcmtldHMvYm91bmRsZXNzLWZlZC1ib25kLWJ1eWluZy1mdWVscy1zdG9ja3MtcmVib3VuZC1kb2xsYXItcmVjb2lscy1pZFVTS0JOMjFBM1pO0gE0aHR0cHM6Ly9tb2JpbGUucmV1dGVycy5jb20vYXJ0aWNsZS9hbXAvaWRVU0tCTjIxQTNaTg?oc=5

2020-03-24 16:52:45Z

52780680058998

Tidak ada komentar:

Posting Komentar